Background

Last week we attended Citi’s Global Property CEO Conference in Miami, followed by a tour of CBD office properties in Manhattan. Prior to the conference, we visited Equity Lifestyle Properties’ RV, manufactured housing assets, and Kimco retail properties in South Florida. At the conference, discussions quickly turned to politics, particularly the impact of the Trump administration’s decisions on markets. In 45 meetings with real estate management teams, topics such as tariffs, federal workforce job cuts, and proposed Medicaid cuts dominated early conversations. Despite this volatility, management teams and investors were more optimistic about the global commercial real estate outlook, with markets, lenders, and buyers adjusting to the current interest rate environment. Many expect this to lead to a more active transaction market in 2025.

Following our meetings, fundamentally, we remain optimistic about Data Centers (DC), despite the recent correction, Sunbelt Apartments, Single-Family Rentals (SFR), and Industrials. We are cautious on Storage fundamentals and Senior Housing (SHOP) valuations despite very strong supply/demand fundamentals. We came away thinking that the Life Science sector is one to keep a close eye on and to reverse our underweight at some point, although timing is difficult.

Big Picture Takeaways

Real Estate Transaction Markets Improving

In our note from the November 2024 Nareit Las Vegas Conference, the US 10-year Treasury yield was around 4.45%. By the Miami Conference, it had dropped to 4.25%, with expectations of further Fed rate cuts later in the year. This slightly lower rate environment is encouraging commercial real estate transactions. Meanwhile, high labor and construction costs have made development less attractive, prompting many groups to focus on acquiring assets below replacement cost. In the week leading up to the conference alone, US REITs announced USD 9.5bn in transactions. Notable deals included Welltower’s USD 3.2bn acquisition of a Canadian SHOP portfolio, Sun Communities’ USD 5.65bn all-cash sale of its marina portfolio to Blackstone, and Avalon Bay’s USD 620m purchase of Texas Class B+ apartments. Following our meetings, we believe buyers and sellers are finally adjusting to the current rate environment, and we expect an uptick in transactions and M&A activity throughout the year.

Tariffs

President Trump’s plan to implement reciprocal tariffs globally could have mixed impacts on REIT sectors. Some, like timber and residential, may benefit, while others, such as industrial and retail, could be negatively affected. Tariffs on steel, aluminum, lumber and other construction input materials could raise costs to develop new commercial properties. As construction costs increase and new developments slow, a supply-demand imbalance should benefit existing property owners. REITs with significant development exposure could be hurt by higher costs.

Tariffs may also disrupt global supply chains, impacting REITs reliant on international tenants or global trade. Industrial REITs, especially those in logistics with properties near ports, could see reduced trade, while retail REITs may struggle if tariffs decrease demand for consumer goods.

Timber REITs have outperformed the broader REIT index this year, largely due to expected tariffs on Canadian timber, which has driven up U.S. lumber prices. However, the main driver for lumber demand is new home construction and remodeling. While higher lumber prices may boost REIT performance, they could also discourage builders from starting new projects or homeowners from pursuing large remodeling plans.

Federal Layoffs

Some investors at the conference raised concerns about the impact of the Trump administration's efforts to reduce the federal workforce. Tens of thousands of federal jobs were cut in the first two months of his presidency, with total job losses potentially reaching hundreds of thousands this year, which would be one of the largest layoffs in U.S. history. Investors are particularly concerned about the effects on residential and office properties in Washington, D.C.

Residential REITs Avalon Bay (AVB) and Camden Properties (CPT) each derive about 7% of their total NOI from D.C. Both CEOs noted that these markets remain healthy, with no signs of declining tours or occupancy. However, with federal layoffs just beginning and likely to increase, we anticipate that continued job cuts under the Trump administration could weaken residential demand in Washington, D.C. in the coming years.

The impact of DOGE cuts on D.C.’s office market is less clear. One the one hand, DOGE is preferentially cutting bureaucratic functions, which is leading most of the job cuts to be concentrated in D.C. On the other hand, remaining federal workers will be called back into the office, which some REIT management teams speculate will increase office attendance amongst government contractors as well.

Medicaid Cuts and the Nursing Home Industry

At the conference, we met with skilled nursing facility (SNF) REITs Omega Healthcare (OHI), Sabra (SBRA), and American Healthcare REIT (AHR). Stays by elderly residents at these facilities are primarily funded through Medicare and private pay, with longer stays covered by Medicaid. Medicaid is a joint federal/state government program that provides health coverage to low-income individuals and families, including children, elderly adults, and people with disabilities. Republican lawmakers have proposed substantial Medicaid cuts to reduce federal spending, raising concerns that lower reimbursement rates for SNF operators could harm an already low-margin industry, potentially reducing rent coverage and impacting REITs' ability to collect full rent, as seen during the COVID-19 pandemic.

As a result, SNF REITs have underperformed both other healthcare REITs and the broader market this year. When we asked the REITs about potential impacts, they outlined scenarios ranging from minimal cuts (affecting only non-elderly Medicaid funding) to per capita caps which would seriously limit the amount of federal funding that states receive for Medicaid beneficiaries on a per-person basis (most bearish scenario – but most unlikely). While it’s difficult to predict the outcome, we believe the Republican Party may avoid cuts to elderly care, focusing on younger populations instead, which would likely have limited impact on SNFs. In response to Medicaid uncertainty, OHI has increased rent coverage requirements for SNF acquisitions to 1.4x EBITDAR (up from 1.2x), a 17% increase.

Sector Takeaways

Life Science

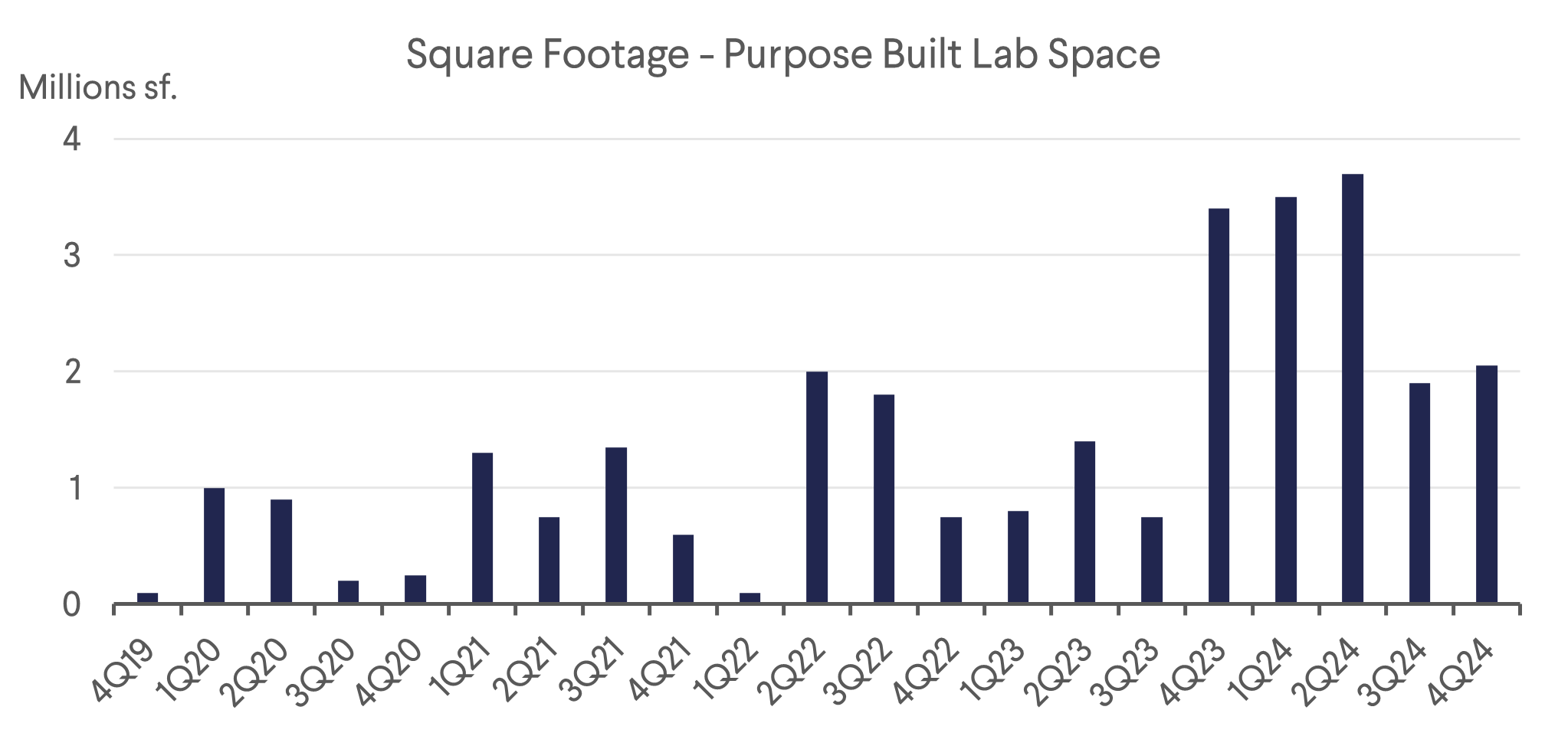

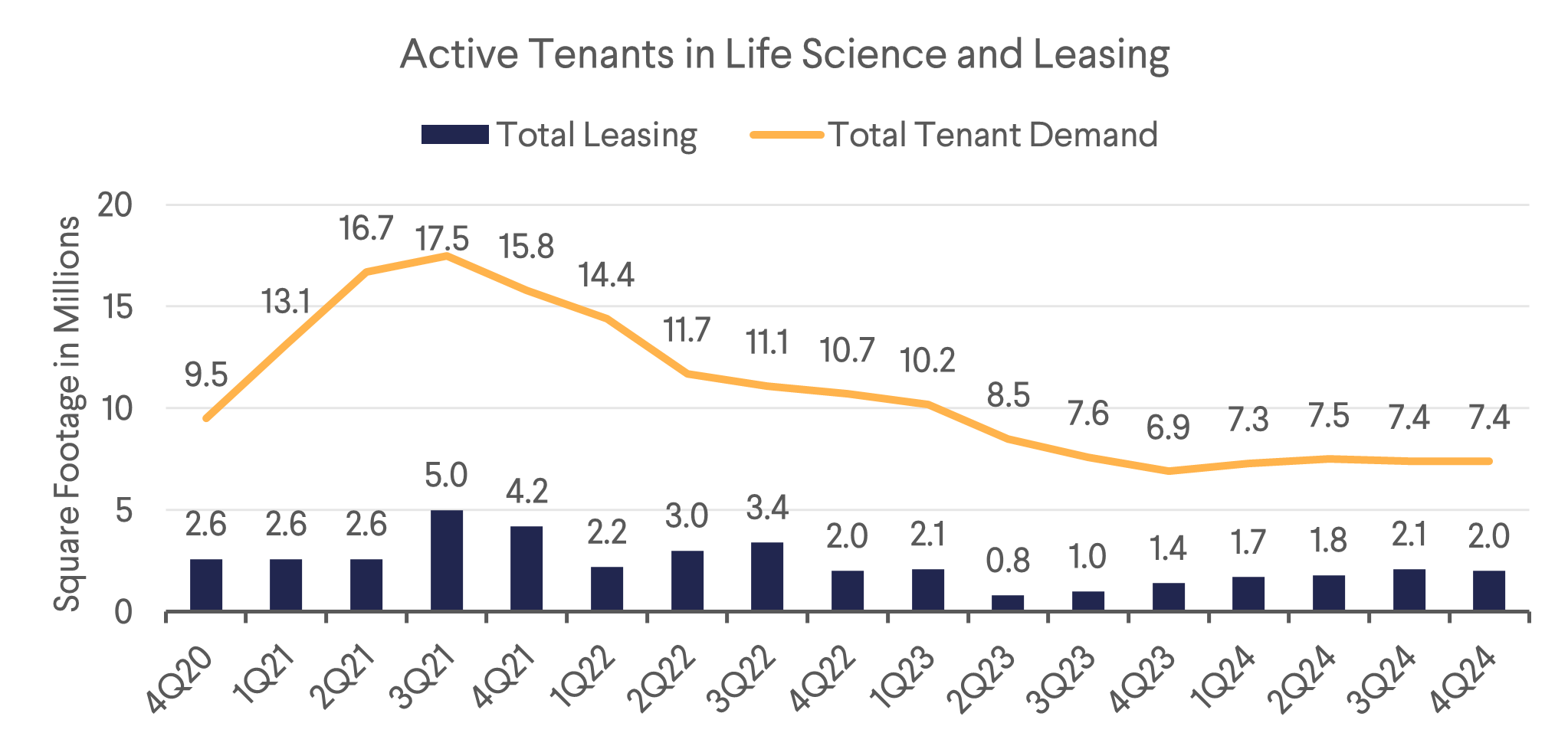

For nearly three years, chronic oversupply in the Life Science markets of Boston and San Francisco has hurt REITs in the sector. Alexandria Real Estate (ARE), the first and only pure-play Life Science REIT, has seen its stock drop 55% from its peak in late 2021. Developers overbuilt while Life Science tenants, like biotech and pharmaceutical companies, scaled back spending and leasing as the sector slowed post-pandemic, with many companies also enacting layoffs in 2024.

After speaking with pure play Life Science REIT, Alexandria Real Estate, and Healthpeak Properties (which derives 39% of its NOI from Life Science), we believe supply peaked in 2024 and fundamentals have bottomed. While significant supply will still enter a weak market in the first half of this year, we expect vacancies to decline as new supply delivers at a more normalized level, with key performance indicators accelerating in 2026.

Demand in 2025 could surpass expectations, as tenant demand and leasing, which bottomed in Q4 2023, have since stabilized. DOC's CEO expects that falling supply, along with lower interest rates by 2H 2025 and into 2026, could boost demand by stimulating VC funding and IPOs in biotech and pharma, leading to increased hiring and greater space needs for new entrants. Both DOC and ARE believe their shares are undervalued and have authorized $500 million share buybacks (2.9% of ARE’s market cap and 3.6% of DOC’s), which they have actively executed since late 2024.

Data Centers (DCs)

Across six meetings with five executive teams managing global DC portfolios, we obtained updates and additional context on a variety of topics, including power availability, the resurgence of China tech and growth of China AI, hyperscale demand vs. enterprise demand, and AI training vs. inference.

On the topic of power availability, we learned that “time to power,” the lead time for delivering electricity to a new DC facility, is a bit shorter in LatAm markets, but likely to remain elevated in the traditional Tier One markets for several years. In addition to long “time to power” in Tier One markets, we learned that supply chains for key components such as UPCs, generators, and natural gas turbines are still the worst they’ve ever been. Four-to-five-year lead times are common for some of the most important parts of a data center. While DC executives said that AI inference is likely farther away than most people think, they confirmed it is almost certain to play out the way we think it will – leading to increased demand in Tier One markets, which are close to GDP and population centers. Management teams were also positive on the impact of DeepSeek on Chinese AI spending and sentiment.

Given recent headlines about Microsoft potentially pulling back on Data Center leasing, some investors in our meetings with DC management teams were predictably nervous about the outlook for hyperscale demand. One management team was insistent that these headlines are driven by shifting dynamics in OpenAI’s relationship with Microsoft following OpenAI’s announcement of their Stargate DC partnership with Softbank and Oracle. Indeed, the day after the conference ended, Bloomberg reported that OpenAI and Oracle will be installing 16,000 Nvidia GPUs in Abilene, TX this summer, with an additional 48,000 GPUs expected at this campus by end of 2026. Like Oracle, Facebook parent META is also ramping up its DC spending, and investors should be aware that, in addition to the traditional hyperscalers, newer enterprises such as Uber and TikTok require similarly large blocks of capacity for their operations. While we are not as nervous as some investors regarding hyperscale demand, we have always preferred owner-operators of network-dense colocation facilities, like Equinix and SUNeVision, both relative outperformers this year in the DC space, and both core holdings in B&I funds.

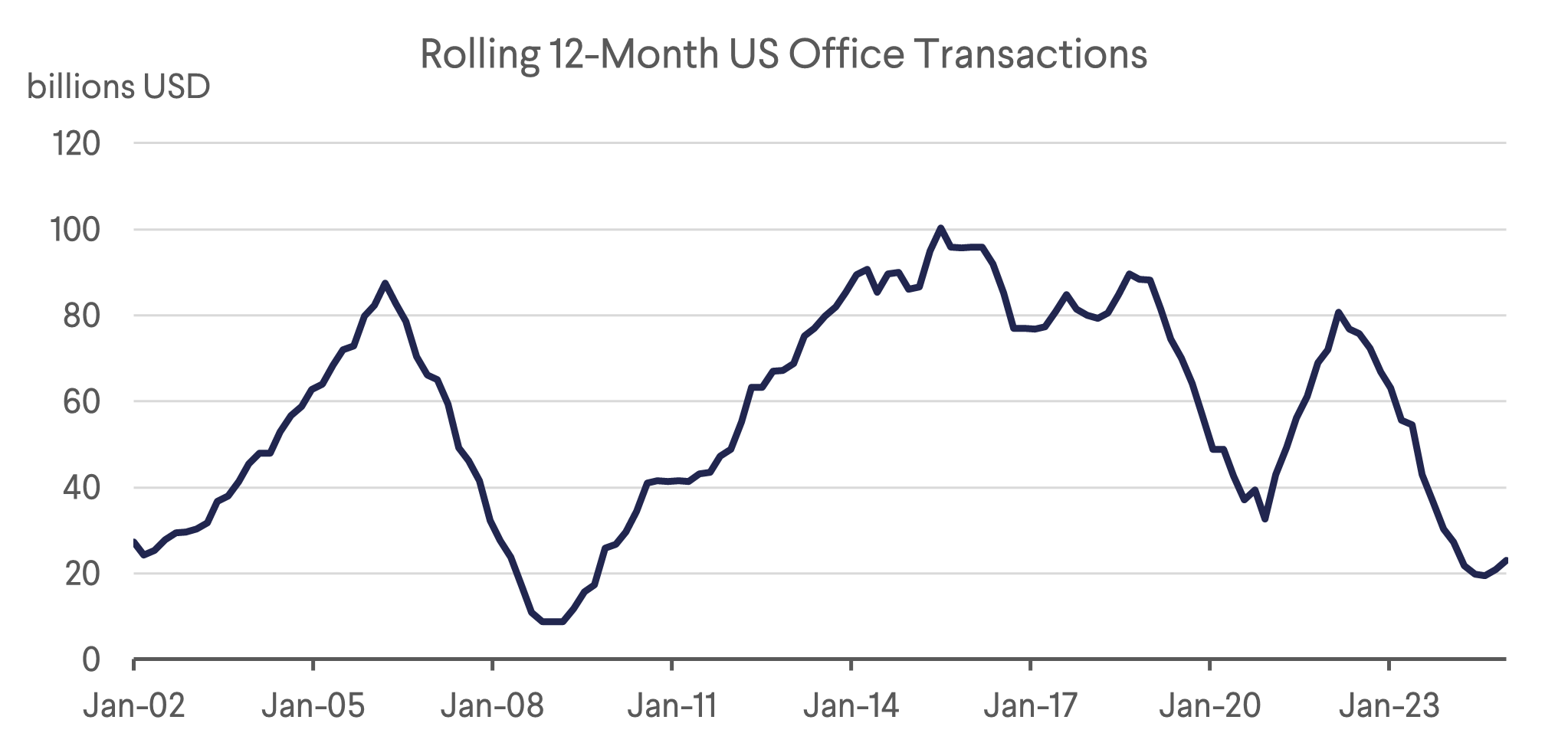

Office

Office REIT management teams were the most upbeat we’ve seen in several years. Office attendance continues to pick up as “RTO” mandates take effect across the country. One CEO informed us that Amazon, whose RTO mandate took effect in January, has a shortage of approximately 20,000 desks nationwide. For the last couple of years, Office REITs have been hoping for an opportunity to repeat their post-GFC playbooks of acquiring trophy assets. Some Office REITs were able to close deals in Q3 of last year, and we’ve seen more deals coming through in Q4 and into 2025. We expect this trend to continue, driven by two ongoing themes: (1) lending markets, and especially CMBS, are re-opening for the office sector after a two-to-three-year pause, and (2) selling pressure from large allocators in the insurance and pension spaces looking to reduce their direct investment exposures to US Office.

During the conference, Sunbelt Office REIT Highwoods (HIW) announced the acquisition of Advanced Auto Parts Tower, a 20-story Class AA tower in the North Hills market of Raleigh. The 100% leased tower has more than eight years weighted average lease term remaining, and is adjacent to another, similarly sized HIW office tower that is 98.4% leased. We estimate a purchase price of c.USD 415/sf. and a cap rate between 7-8% on this deal, which will be immediately accretive to cash flow upon closing within the next 30 days.

Believe it or not, many Office REITs are also finding attractive growth opportunities through ground-up development. New construction starts are effectively nonexistent, and larger users know to plan ahead because high-quality office space takes four years to build. BXP Inc., formerly known as Boston Properties, highlighted its development site at 343 Madison, which will connect directly into Grand Central Terminal. As the only actionable site in the Grand Central submarket, this project has already attracted interest from 6 potential anchor tenants, even though construction on the office tower has not even started and is not likely to finish before 2030. HIW’s 23Springs, the newest office tower in Uptown Dallas, will complete construction this quarter and is already 62% leased, with the first tenants scheduled to move in in June. We believe that demand for high quality office space will never disappear completely, and REIT-owned office space is overwhelmingly trophy quality.

Residential

Our meetings with residential REITs were largely positive, driven by the persistent shortage of affordable housing and growing demand in the US. We toured ELS assets and met with the management team. We would describe the company and investment thesis as a steady compounder. ELS can grow rents by about 5% a year, has a well-covered dividend yield of 3%, consistently grows FFO/sh ~5.5%, and grows their dividend at ~5.5%. Its predictable cash flow and stable renter base contribute to steady stock compounding. The ELS property we visited in South Florida had 662 sites, mostly seasonal and annual RVs, with many tenants being retired French Canadians from Quebec enjoying the sunny weather.

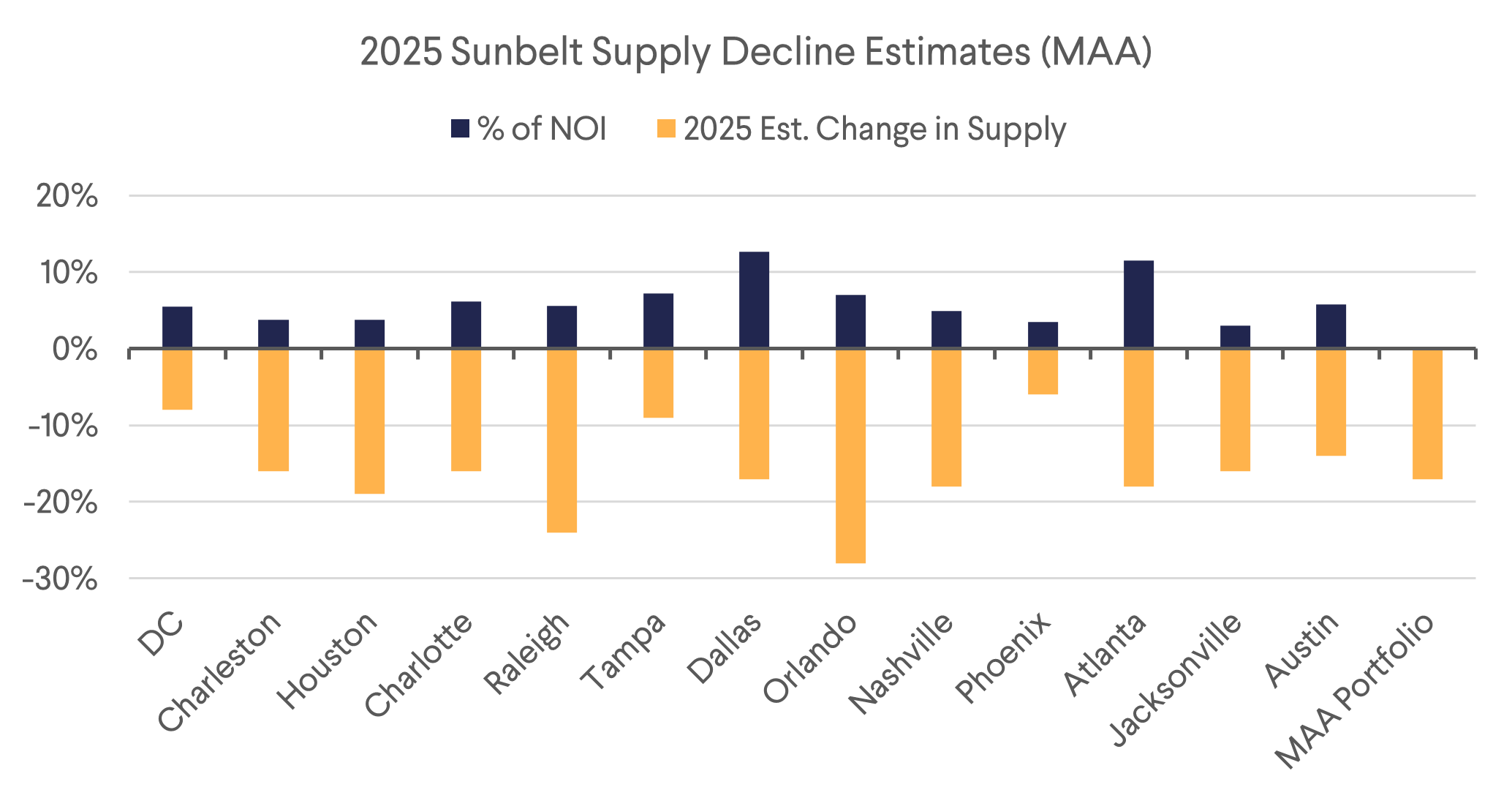

On the Thursday before the conference, AVB, the largest apartment REIT, announced it was purchasing eight Class B/B+ properties in Texas for $620 million at a ~5% cap rate. This move supports our view that as apartment supply dwindles in 2H 2025, Sunbelt apartment REITs like Mid America Apartments and Independence Realty Trust, who are trading at higher cap rate ranges, will see accelerating rental growth, driven by strong population and job growth. We’ve seen this trend reflected in their share prices this year, and their packed meetings at the conference suggest growing investor interest in this space.

Single-family rental (SFR) REITs American Homes (AMH) and Invitation Homes (INVH) have underperformed apartment and MH/RV peers, impacted by increased build-to-rent supply, post-COVID demand normalization, and concerns about a turnover spike from lower mortgage rates that never materialized. INVH’s CEO highlighted that the SFR market thrived from 2012-2021 in a low-interest-rate environment, and we agree that long-term growth is fueled by the lack of affordable homes in the U.S. Many aging millennials with growing families are priced out of homeownership due to down payment issues and high interest rates, leaving renting as their only option. On a P/FFO basis, AMH (19.3x) and INVH (17.6x) are about one standard deviation cheaper than usual compared to peers. SFR rental spreads in 1Q were up 3%, outpacing apartments, making this sector an attractive opportunity given its fundamentals, growth potential, and relative undervaluation.

Asset Tour Pictures

Equity Lifestyle Properties Tour Residential in Fort Lauderdale, FL – 2 March 2025

|  |

Kimco Realty Corporation Retail Tour in Miami, FL – 2 March 2025

|  |

BXP Inc. Midtown Manhattan Office Tour in New York, NY – 6 March 2025

|  |

|  |

Download the PDF version of the report here