Background

REITweek 2026 in New York City brought a noticeably constructive tone across the more than 30 management meetings and property tours we participated in. The conversations centered on real estate fundamentals rather than macro fears, a meaningful shift from where the dialogue stood just a few months ago. Two themes that dominated the Citi Miami conference in March, the geopolitical overhang from Iran and fears that AI would trigger mass white-collar layoffs, were not a frequent topic of conversation in NYC.

What we did hear a lot about was that low supply is finally starting to become a positive driver to pricing and that there is an inflection in demand in certain sectors that were beaten down.

On geopolitics, US equity markets have largely shrugged off the Iran conflict. REITs, which are long-duration assets sensitive to sharp moves in rates, recovered from the initial sell-off and are now moving higher in a weaker market as investors look through higher rates to the increasingly positive supply/demand fundamentals.

On AI, the conversation has shifted materially. Discussion of white-collar job destruction and its knock-on effect on office and residential demand was minimal. Management teams and investors alike appear to have landed on a more optimistic view. AI is disruptive, but not the mass-employment destroyer the headlines predicted. We heard more about how AI was positively impacting demand for real estate (and not just Data Center REITs). For example, AI startups are absorbing office space in NYC that would otherwise sit vacant, and the AI build-out is generating incremental industrial demand.

Meanwhile, REITs have quietly outperformed the S&P 500 year-to-date, a reversal that has gone under-appreciated in the broader market. The outperformance reflects a powerful dynamic: after years of being universally underweight in asset allocation strategies and reaching historically wide relative valuation discounts to equities, it does not take much positive news and capital rotation to move the sector. Falling new supply across nearly every REIT property type is now the central bull thesis, and management teams are increasingly confident in the fundamentals supporting their businesses.

Big Picture Takeaways

Broadening Sentiment & Performance as Supply Picture Improves

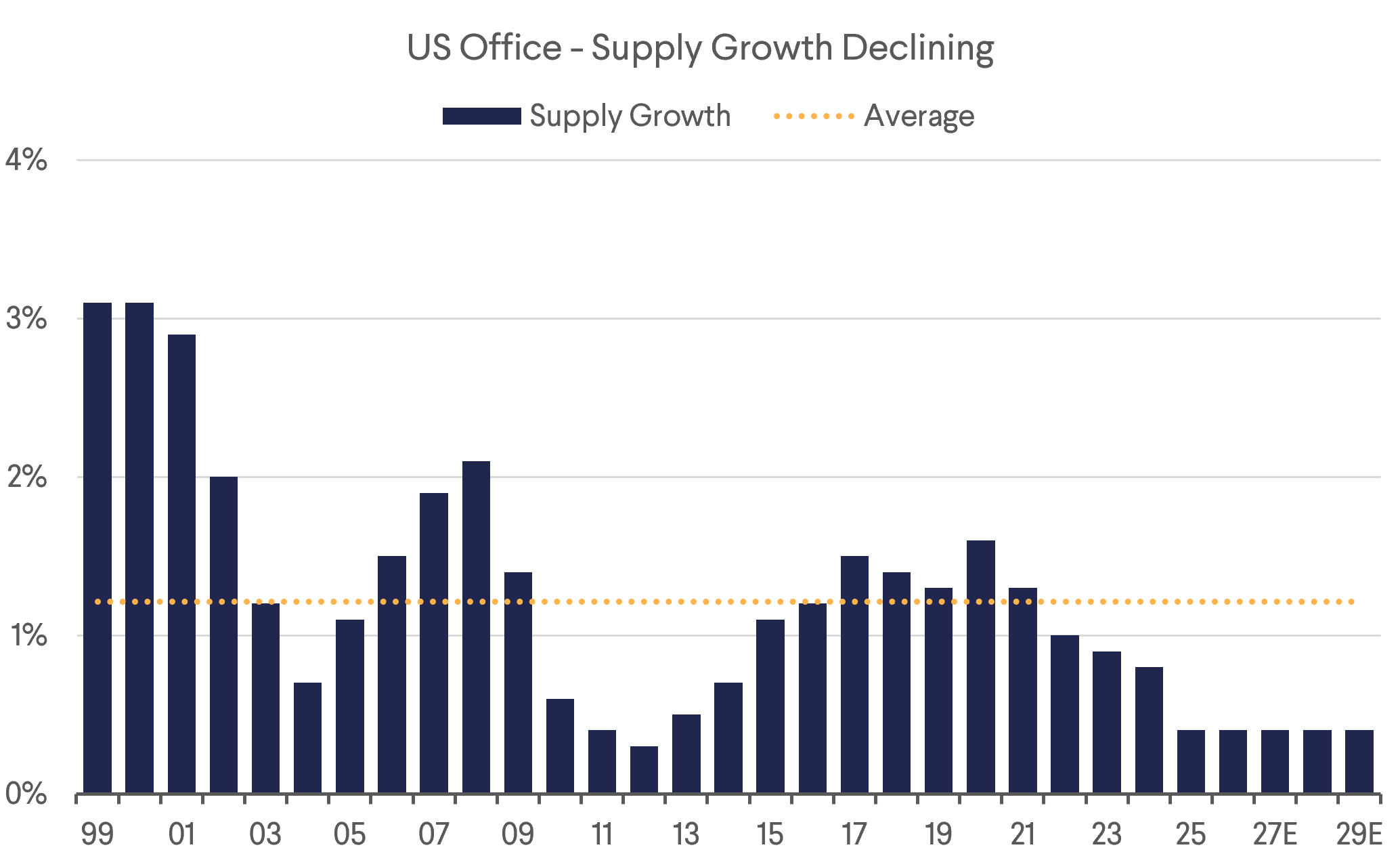

Performance within the REIT index has broadened YTD. Office, Apartments, Self-Storage and Industrial, sectors that have spent the past few years absorbing excess supply, are steadily improving. The common driver is one we have been highlighting for some time now; new supply is falling significantly. What was a thesis two years ago was the main conversation point in our meetings and tours in New York. Management teams across the board confirmed that the narrative is taking hold, and the sectors that struggled longest are finally seeing improved pricing power.

New supply is difficult to underwrite due to numerous inputs: construction costs are materially higher than pre-pandemic levels, labor costs have not come back down, material costs remain elevated due to supply chain disruptions and tariffs, and, most decisively, the increase in interest rates has raised the discount rate to the point where many projects simply do not pencil.

Sectors that previously attracted waves of speculative development including Office, Industrial, Apartments, and Self-Storage, are where the math is most punishing and developers have responded accordingly. Higher-for-longer rates, while a headwind to refinancings, are perversely supportive of most real estate fundamentals. They choke off new starts and temper private-buyer competition, putting a floor under cap rates. In Retail, PECO estimates market rents need to rise 30-40% before new development pencils. In Sunbelt Apartments, concessions are finally burning off. In Office, no meaningful new supply is expected in 2028/29.

The K-Shaped Economy

The divergence between top and bottom US consumer cohorts continues to widen and REIT management teams are acutely aware of the fault lines. The lower-income consumer is stressed on multiple fronts. Elevated gasoline prices are compressing disposable income, stubborn shelter inflation continues to eat into real wages, and the residual effects of pandemic-era price increases have not unwound while wages have stalled. The upper-income consumer, by contrast, remains healthy. This cohort bought financial assets and real assets with Covid liquidity rather than consumer goods and the wealth effect from equity and housing appreciation has kept spending resilient.

The bifurcation is visible in REIT performance and tenant health across sectors. Net-lease names with high exposure to middle and lower-market restaurant and service tenants are feeling it most acutely. Four Corners Property Trust (FCPT), which owns a portfolio weighted toward casual dining and quick-service restaurants catering to the middle and lower market, is navigating tenant coverage pressure as the consumer it serves pulls back on dining out. Same-store rent coverage at FCPT's restaurant tenants has tightened as demand softens, and the cushion between rent obligations and tenant EBITDAR has compressed. In response, FCPT's most recent acquisitions have been of veterinary practices and auto-servicing.

The K-shaped economy is also generating political consequences that are worth watching from a real estate perspective. Widening wealth inequality, particularly in high-cost urban markets, is producing a new wave of populist leadership. New York City's new mayor is Zohran Mamdani, whose platform centers on rent control, tenant protections, and aggressive intervention in the housing market. Whether or not Mamdani's policies are enacted in full, the direction of political momentum in large cities is toward more landlord regulation and higher taxes which could have negative implications for real estate investors and job growth. This is a tail risk for urban multifamily and office and a dynamic we are monitoring closely as it unfolds in America's most important office and apartment market.

Sector Takeaways

Data Centers

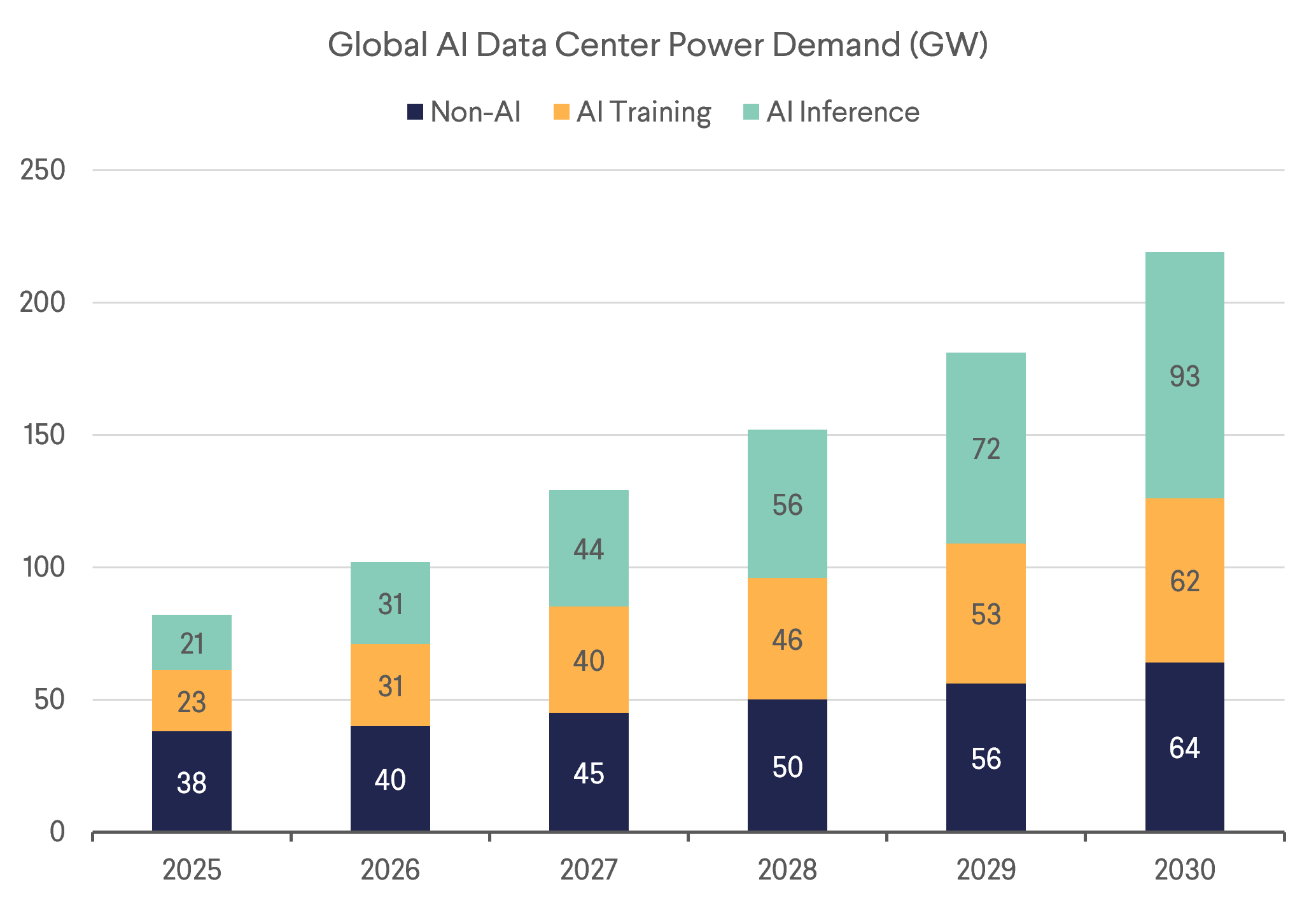

Data Centers, while at risk of an AI pullback, remain among the strongest secular stories in the listed REIT universe as AI inference and agentic computing demand is layering on top of the existing hyperscale cloud infrastructure buildout. The disciplined supply posture of the large public platforms, EQIX, DLR, and AMT's CoreSite, continues to favor incumbents with power access, scale, and pre-leased pipelines. While the sector is benefitting from strong tailwinds, Digital Realty mentioned the high leverage of private peers at 15-20x as their biggest concern.

We met management for the recently IPO'd Blackstone Digital Infrastructure Trust (BXDC), the largest cash-box REIT IPO ever. Cash-boxes are generally viewed critically in the sector, so we wanted to understand why Blackstone chose this structure and the public market. The strategy is to buy stabilised assets leased to the large hyperscalers. In Data Centers you can currently acquire assets on 15-year leases with the best credit tenants (A-rated) at cap rates above 6%, which is attractive relative to other sectors. The cash-box structure lets Blackstone enter quickly without assembling a portfolio pre-listing and, with a USD 25bn pipeline, the vehicle could scale meaningfully as long as the cost of capital allows and BXDC can execute. Cash-boxes are not allowed to engage with sellers ahead of listing, yet in its first days BXDC has already seen elevated reverse inquiries from developers and hyperscalers alike. The first deal announcements will be the key proof point for BXDC, and we are watching closely.

Industrial

Prologis (PLD) pointed to growing signs of an Industrial inflection, with occupancy improving over several quarters, rent growth picking up and constructive leasing activity despite renewed macro uncertainty. PLD argued the sector is starting from a strong base. Vacancy is lower than in previous downcycles and pricing power should return faster if momentum holds. The key drivers remain ecommerce and the professionalisation of the supply chain. The Data Center supply chain has emerged as a meaningful new source of demand, contributing roughly 10% of new total demand.

Views on the largest market, Southern California, were split. Prologis sees it lagging but clearly improving, while Terreno (TRNO) flags the risk that weakness in Los Angeles is more structural, citing a business-unfriendly environment and a struggling entertainment sector. We remain constructive on the sector overall. The combination of improving demand and low near-term supply is starting to show in the numbers.

Healthcare

Despite recent relative share price weakness, as investors have rotated out of healthcare into beaten-down sectors finally coming to life, our Senior Housing Operating (SHOP) meetings still had the best tone of the entire conference.

The average SHOP resident is 85 years old, meaning we are moving into the peak post-WW2 baby boomer wave. This points to 2030 as a peak demand year for the sector and the demographic tailwind is large and still accelerating. Supply cannot respond meaningfully because construction is complex, entitlements are slow, and builders are directing capital toward the data center boom instead. The result is occupancy gains compounding into exceptional operating leverage, with NOI and FFO/share growth that few other property types can match.

Our best meeting of the conference was with American Healthcare REIT (AHR). We expect the company to complete USD 1.2bn of acquisitions in 2026 at going-in cap rates in the high-5%/low-6% range with a value-add path to 7-8% stabilized yields. AHR sports a balance sheet at 3x net debt/EBITDA, and we expect 13% FFO per share growth at the midpoint along with 8% dividend growth in 2027.

During our Welltower meeting the company highlighted their confidence in FCF per share growth as they continue to improve tenant operations in what they see as an antiquated business that has room to improve margins by using WELL's topflight data and operational systems and expertise. The company backed up this confidence with a 15% dividend increase on the Monday starting the conference.

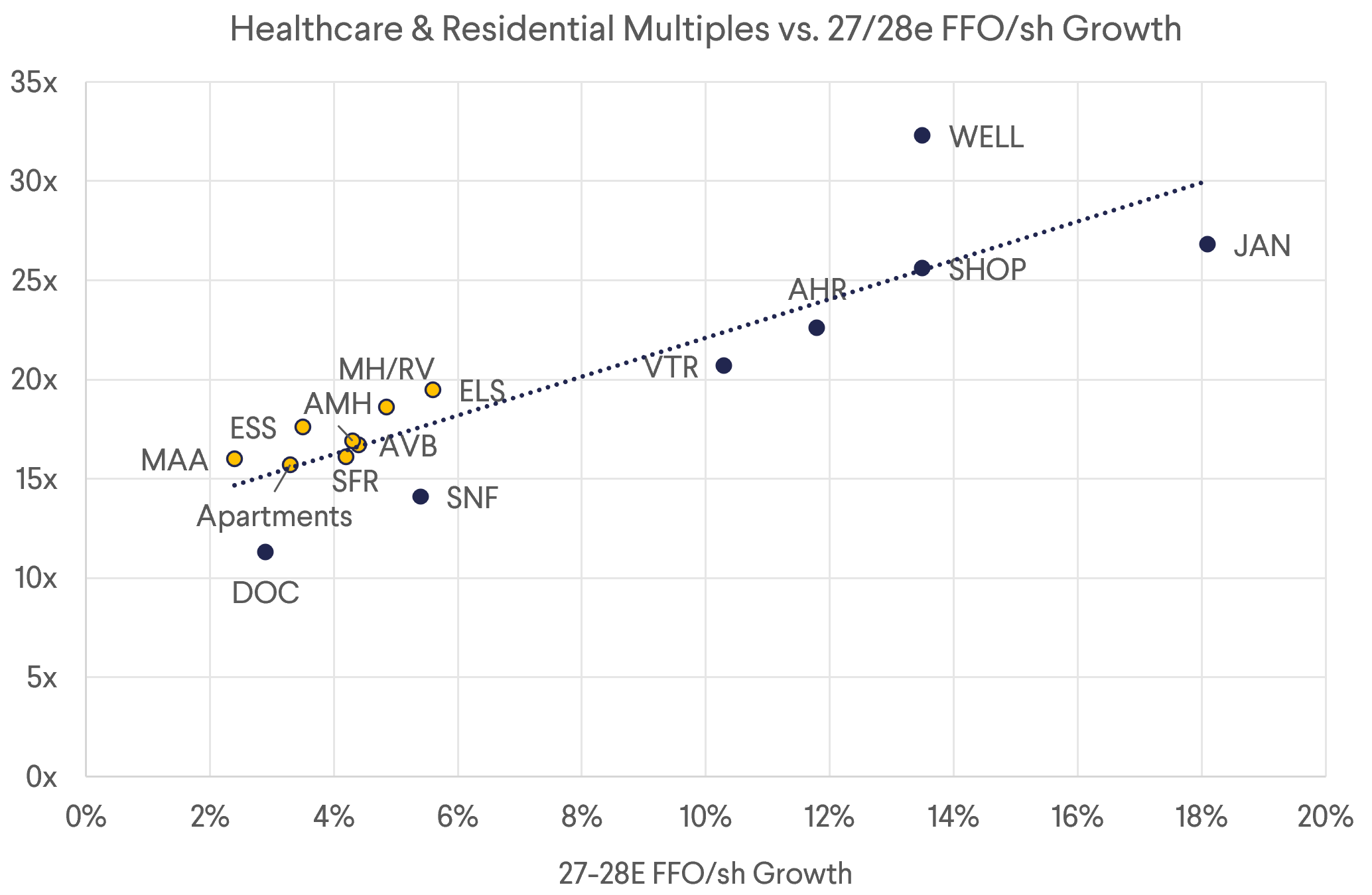

The high multiples Healthcare names trade at are mostly justified by the growth. SNFs trade at c.14x on low-single-digit FFO growth, life science is similarly valued and even weaker, and residential REITs cluster at 15-18x on 2-5% growth. WELL at 32x and JAN at 27x look expensive in isolation, but against 12-18% forward FFO growth driven by supply-constrained occupancy gains and an accretive acquisition pace not included in guidance, the multiples reflect growth at a reasonable price.

The sector is nonetheless getting crowded. Cap rates on marquee SHOP assets have compressed 25-50bps since the start of the year, sub-6% is now becoming more common, and auction processes are becoming the norm. NHI's warning that 'today's applauded acquisition is tomorrow's workout' reflects a genuine concern that mid-tier REITs chasing SHOP exposure are buying at yields that leave little margin for operational underperformance. LTC is acquiring at 7% on sub 10-year old assets and expects deal pace to slow over the next six months. We prefer the larger leaders that have been in the SHOP space for years over healthcare companies chasing the theme without the operational depth, and we are cautious on the 'SHOP-ification' trade among net-lease and SNF REITs converting to RIDEA structures. The debate is whether these are genuine operators or simply capital allocators paying up for a business they are not experts in.

Apartments

Apartments are inflecting nicely into peak leasing season with blended lease growth turning positive across multiple platforms. UDR reported blended growth of +2.4% in May, MAA +1.1% (the best reading in two years), and IRT QTD +1.1%. Concessions in Sunbelt markets are finally burning off though the process is gradual.

Coastal markets still lead the recovery. New York and Northern California are the strongest performers, benefiting from a persistent structural undersupply. The Sunbelt recovery is real but slower. Austin remains softer, and IRT is an active seller of Denver given its negative read on Colorado's regulatory environment. The fear that AI-driven job losses would crater apartment demand has not materialized in leasing data. The preferred capital allocation decision across the sector is still buybacks, reflecting the view that shares in many cases trade well below NAV and at a discount to private peers.

Office

We left our Office meetings positive and glad we had added SL Green (SLG) to the portfolio in March. The feeling is that the sector has clearly turned. The fear of AI-driven white-collar job destruction that drove the sector's sharp underperformance into early 2026 has not materialized in tenant leasing behavior. Feedback was unanimous across our meetings with BXP, KRC, ESRT, and SLG—no tenant is cutting space because of AI, and AI companies are in fact absorbing space as their companies go into growth mode.

We toured One Vanderbilt, SLG's Class A+ trophy tower built adjacent to Grand Central Station in the Park Avenue submarket and saw the demand and energy firsthand. The Park Avenue submarket availability sits at only 4%, hedge funds and PE firms are actively expanding, and the new JPMorgan headquarters has reinforced the corridor as the most sought-after office address in the US and arguably the world. SLG described it as the deepest market it has ever seen. SLG has 50% of its portfolio within a five-minute walk of Grand Central, 9m sf of leasing activity in its pipeline, an embedded mark-to-market of 25%, and SS cash-NOI growth of 10% expected in 2027. SLG's position sitting directly above Grand Central with the Long Island Rail Road and multi-line commuter rail access is an incredible locational advantage that is difficult to replicate. Concessions remain elevated at USD 125/sf TI on 10–15-year terms, but face rents are moving up quickly and net-effective rents are rising. We believe the SLG earnings inflection is real but is primarily a 2027 story, as leased-but-not-commenced space takes time to burn off free rent and convert to cash flow.

In the Sunbelt, Cousins Properties (CUZ) is the clearest expression of the recovery: tenants are upsizing, the flight-to-quality trade is active in their trophy assets, and corporate relocations to Dallas, Atlanta, and Austin continue to support demand. CUZ told us they are targeting 90% occupancy by the second half of 2026 with no meaningful new supply expected until 2028/29.

Shopping Centers

Supply constraints continue to support rent growth in retail. Phillips Edison (PECO) estimates market rents need to rise 30-40% before new development pencils. The transaction market was a key theme in our meetings. US retail property transaction volume rose 26% to USD 71.6bn last year according to MSCI, with the highest level of activity from institutional investors and public REITs since 2016. Grocery-anchored retail remains the most favoured asset type, but investor interest is broadening to unanchored strip centers, power centers and lifestyle centers.

On the listed side, Curbline (CURB) has specialised in unanchored strips and built a platform to source a high volume of deals, targeting USD 850m of acquisitions in 2026. With leasing and transactions both strong, retail REITs continue to perform well. Compressing cap rates and higher debt costs could make it harder to source attractive deals, yet management teams still sounded confident of hitting full-year acquisition guidance and are on track on YTD volumes.

Asset Tour Pictures

SL Green (SLG) Tour of One Vanderbilt – 1 June 2026

|  |

|  |

Download the PDF version of the report here